|

JOIN OUR MAILING LIST |

|

Assessments / Blog 2019-03-18 ES #F Demand with lower volume

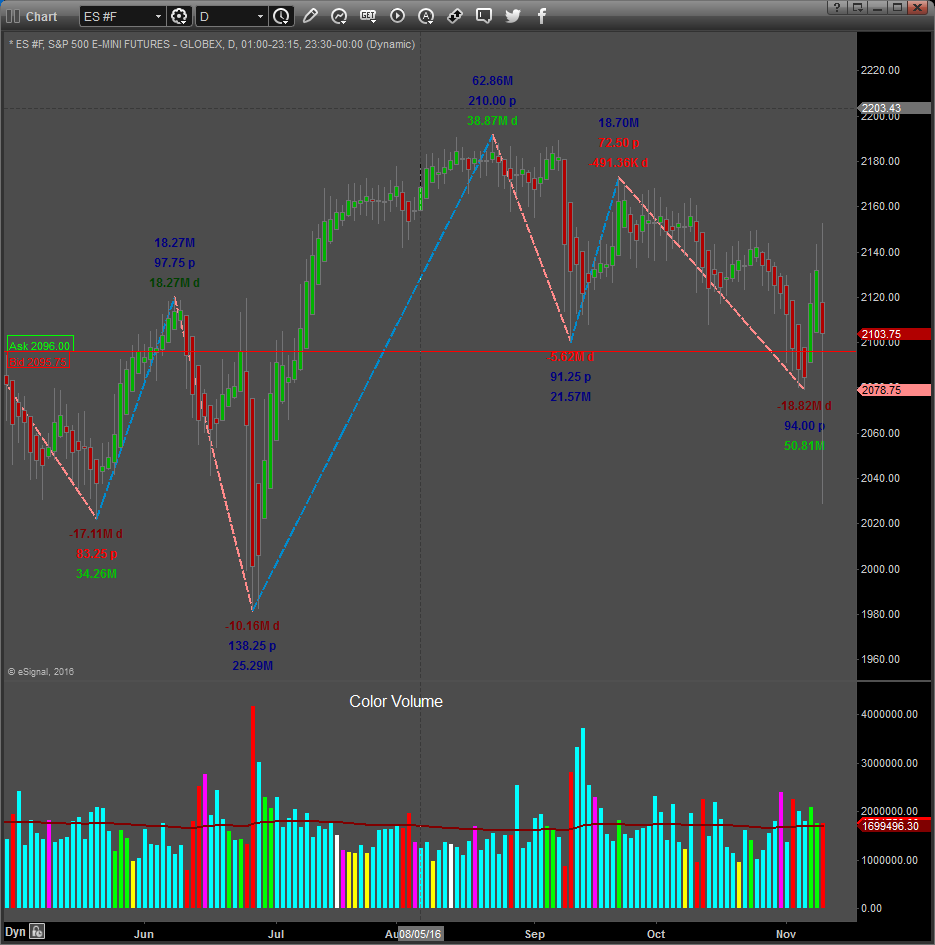

Demand had the upper hand on Friday, making a new swing high. The ES closed higher by 17.50-points. All signals are Bullish, except for daily volume which has been declining for the last 4 sessions in the current up move? In our view the near term and intermediate term is still Bullish. Any pullback below 2782.50 can potentially threaten the near term advance. End of the day Signals March the 15th: S & D Dashboard Algorithm turned Bullish, although Average Volatility Increased Daily Signals changed to the upside These readings are an independent assessment of the one and only measureable fundamental market mover: SUPPLY and DEMAND. It does not matter if price is influenced by a geopolitical event, seasonality, fundamental economic data releases or sentiment driven news, etc. It all reflects in Supply and Demand, the “footprints” of the “Big Boys” or “Smart Money”. Caution: Average Supply/Demand Volatility Increased on Friday and the Transportation Indexes weakened, which will lead to a pullback if the weakness continues. Link to Facebook Group where these assessments are also posted regularly. Links to recent research posts: CHINESE DATA HAS DELAYED EFFECT ON GLOBAL EQUITIES MARKETS – PART III

In the previous two segments of this research post PART I, PART II, we’ve hypothesized that the recent Chinese economic data and the resulting global shift to re-evaluate risk factors within China/Asia are prompting global traders/investors to seek protective alternative investment sources. Our primary concern is that a credit/debt economic contraction event may be on the cusp of unfolding over the next 12~24 months in China/Asia. It appears that all of the fundamental components are in place and, unless China is able to skillfully navigate through this credit contraction event, further economic fallout may begin to affect other global markets. One key component of this credit crisis event is the Belt Road Initiative (BRI) and the amount of credit that has been extended to multiple foreign nations. We don’t believe China will run out money by the end of March and we don’t believe any crisis event will come out of nowhere to land in China within a week or two. Our concern is for an extended downturn to decrease economic opportunity by 5~12% each year for a period of 4~7+ years. It is this type of extended economic slowdown that can be the most costly in terms of political and economic opportunity. An extended downturn in the Chinese and Asian economies would create revenue, credit, debt, and ongoing social servicing issues. Click on this link to read more.... BEST PRECIOUS METALS INVESTMENT AND TRADES FOR 2019

In short, I feel precious metals should be a part of everyone’s portfolio as a long-term hedge and investment. I see precious metals as an insurance policy in case all hell breaks loose in the financial system and we need to fall back to something with physical value for a short period of time. With that said, I am a firm believer that you should never overload in one particular investment or asset class. But I do feel certain metals should have a heavier weighting based on their current potential. The more upside potential the more of that metal you should own shares or physical bullion. Click on this link to read more....

|